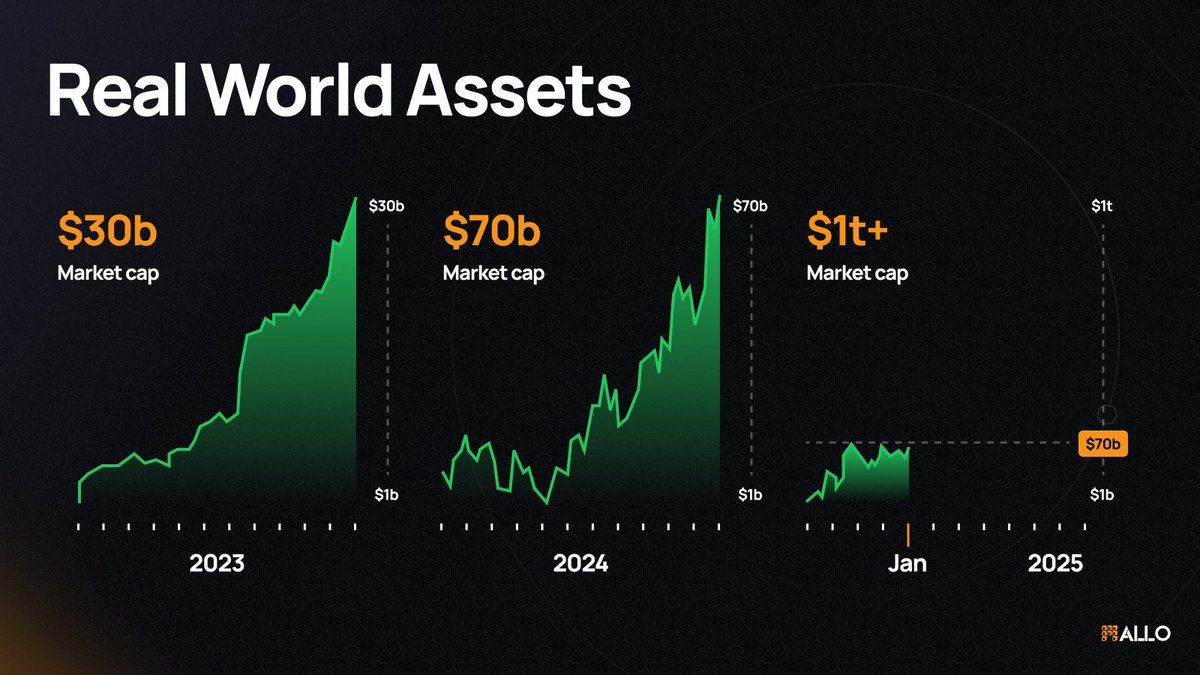

What is RWA prime brokerage

RWA prime brokerage is the convergence of traditional prime services with on-chain tokenized assets. It bundles custody, margin lending, and securities lending into a single interface for institutional investors managing hybrid portfolios. The model allows hedge funds and asset managers to treat tokenized treasuries, private credit, and real estate with the same operational rigor as equities or fixed income.

At its core, this model solves the fragmentation problem. Without it, a fund must maintain separate custodians for its bank deposits and its on-chain holdings. RWA prime brokerage consolidates these functions. It provides a single point of access for borrowing against tokenized assets, executing trades across centralized and decentralized exchanges, and receiving consolidated reporting.

The value proposition centers on efficiency and risk management. By tokenizing real-world assets, institutions can access 24/7 liquidity and programmable settlement. Prime brokers mitigate the new risks associated with smart contracts and chain fragmentation by providing institutional-grade custody and compliance layers. This allows funds to leverage tokenized assets without sacrificing the regulatory oversight required by traditional finance.

Margin financing for tokenized treasuries

Use this section to make the RWA Prime Brokerage decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Rehypothecation controls on-chain

Traditional prime brokerage has long operated on a model of full rehypothecation. When a hedge fund posts collateral, the prime broker often reuses those assets to finance other clients or secure its own balance sheet. This practice maximizes leverage but introduces significant regulatory friction. Under Basel III rules, rehypothecated assets typically carry a 100% Risk-Weighted Asset (RWA) charge, forcing banks to hold substantial capital against them. This capital drain limits the prime broker’s ability to expand financing services, creating a bottleneck for large-scale institutional clients.

On-chain prime brokerage offers a structural solution by embedding granular control directly into the smart contract. Instead of blanket permissions, funds can explicitly approve or deny the rehypothecation of specific tokenized assets. This transparency allows institutions to isolate high-quality collateral from risky lending activities, effectively reducing the RWA charge associated with those assets. The result is a more efficient balance sheet that supports higher leverage without proportional capital costs.

This level of control is not merely theoretical; it is being implemented by leading on-chain infrastructure providers. By treating collateral as a programmable asset rather than a static deposit, these platforms enable funds to optimize their capital efficiency in real-time. For institutions navigating strict regulatory environments, this capability transforms prime brokerage from a passive custodial service into an active balance sheet optimization tool.

Liquidity pools for private credit

Institutional prime brokers are moving beyond simple securities lending to create dedicated liquidity pools for tokenized private credit and real estate. This model addresses the primary friction point for hedge funds: the inability to exit illiquid positions quickly without triggering fire-sale discounts or breaching fund lock-up terms.

By tokenizing assets like warehouse lending facilities, prime brokers can offer secondary market access. For example, platforms like RWA.xyz have tokenized deposits into Democratized Prime, a facility for HELOCs originated by Figure Technologies. These tokens represent fractional ownership in the underlying credit pool, allowing funds to trade exposure on-chain rather than waiting for traditional quarterly redemption windows.

The mechanism works by pooling these tokenized assets into a liquidity layer that prime brokers manage. Hedge funds can deposit their illiquid private credit positions into this pool in exchange for liquid tokens. They can then sell these tokens to other institutional buyers on the secondary market, effectively unlocking capital that was previously trapped in long-dated loans.

This integration reduces counterparty opacity, a known risk in traditional prime brokerage relationships. Instead of holding opaque, non-standardized loan agreements, funds hold standardized digital tokens with transparent ownership records. This clarity allows prime brokers to offer more competitive margin rates and faster settlement times, bridging the gap between traditional finance settlement cycles and the speed of digital asset trading.

Managing wrong-way risk in RWA prime brokerage

The Basel Committee on Banking Supervision (BIS) has long flagged wrong-way risk (WWR) as a critical vulnerability in prime brokerage. The concern is straightforward: a prime broker faces heightened exposure when a hedge fund’s default coincides with a drop in the value of the collateral the fund has pledged. In traditional finance, this risk is often obscured by opaque reporting structures. For tokenized real-world assets (RWA), the stakes are similar but the mechanics differ, requiring a shift from trust-based reporting to verification-based monitoring.

In the RWA prime brokerage model, opacity is the primary enemy. When a fund holds tokenized bonds, real estate, or private credit, the prime broker must know exactly what is in the vault to price the margin correctly. If the underlying asset’s liquidity dries up or its legal status is challenged, the collateral’s value can vanish overnight. This is the essence of WWR—the risk that the counterparty’s failure is correlated with the collateral’s failure. Without transparent, real-time data, a prime broker cannot accurately calculate haircuts or initiate liquidations before the position becomes underwater.

On-chain ledgers solve this opacity problem. Unlike traditional custodial statements that may lag by days or weeks, blockchain-based RWA structures provide a single source of truth. The prime broker can monitor the exact composition of the fund’s collateral in real time. This visibility allows for dynamic margining, where loan-to-value ratios adjust automatically as the RWA’s market price or liquidity profile changes. It transforms risk management from a retrospective audit into a proactive control mechanism.

The result is a more resilient prime brokerage structure. By eliminating the information asymmetry between the fund and the broker, the risk of sudden, unanticipated losses is significantly reduced. This transparency is not just a technical feature; it is a regulatory necessity. As banks integrate RWA into their balance sheets, the ability to prove that collateral is liquid, legally enforceable, and accurately valued becomes the foundation of the business model.

Key questions on RWA prime services

Institutional adopters often face friction when bridging traditional prime brokerage infrastructure with tokenized real-world assets. Clarifying regulatory definitions and operational scope is essential for risk management and capital efficiency.

No comments yet. Be the first to share your thoughts!