RWA prime brokerage in 2026

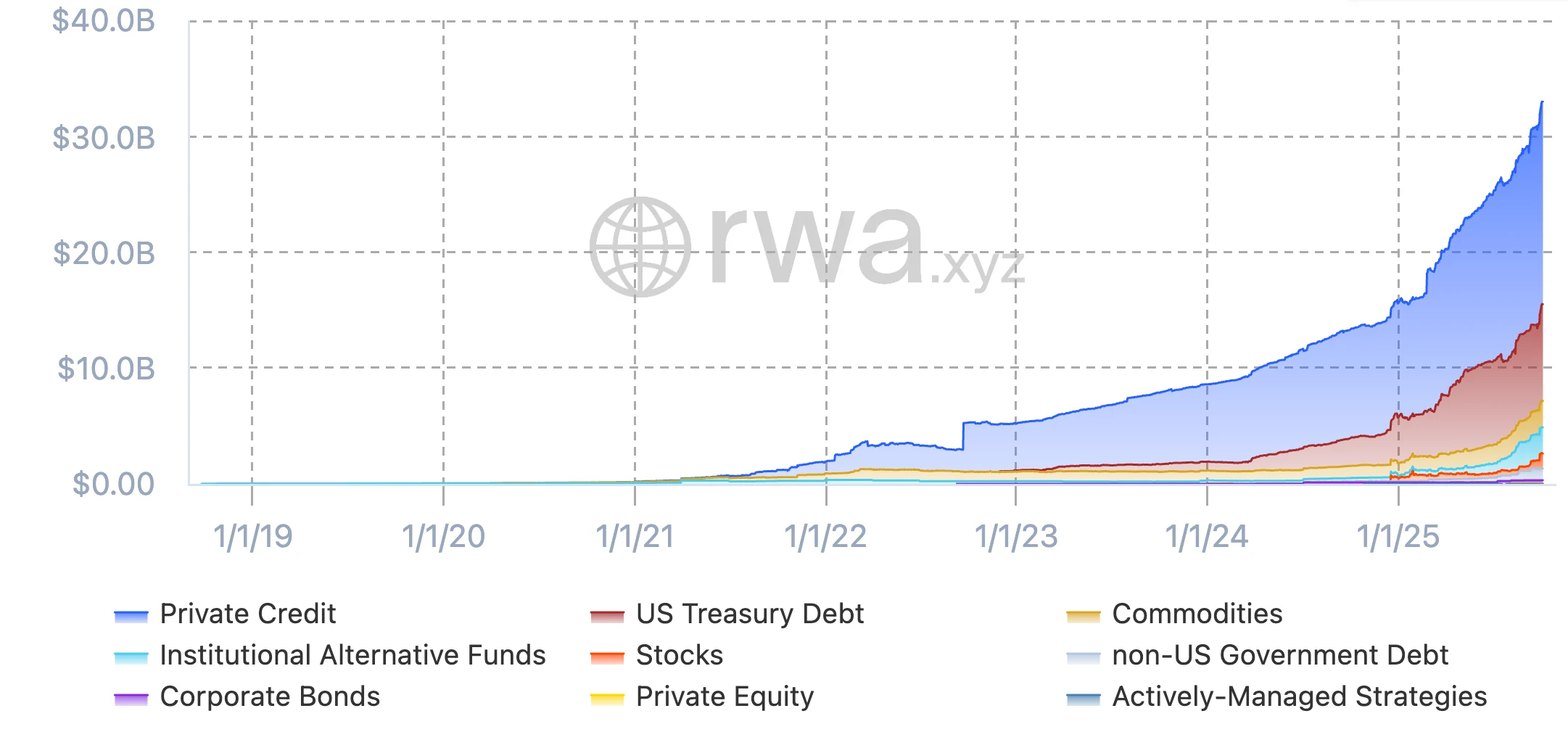

The shift from issuing assets to managing them has arrived. Tokenized stocks have grown from roughly $280 million in mid-2025 to $1.46 billion by May 2026, while RWA perpetuals hit $524.79 billion in Q1 2026 trading volume [src-serp-1]. This surge past the $10 billion mark signals that prime brokerage is no longer a niche experiment but a core infrastructure layer for bridging traditional finance and decentralized liquidity [src-serp-2].

Prime brokerage in this context acts as the central clearinghouse for real-world assets. It provides the collateral management, leverage, and settlement services that allow institutions and sophisticated retail traders to interact with tokenized treasuries, real estate, and private credit. Without these services, the liquidity gap between on-chain efficiency and off-chain compliance would remain too wide for mass adoption.

The market structure is evolving quickly. Traders now expect the same speed and capital efficiency they see in crypto derivatives, but backed by regulated on-chain collateral. This convergence is driving demand for platforms that can seamlessly integrate traditional clearing mechanisms with decentralized exchange protocols. The question is no longer if RWA prime brokerage will scale, but which providers can handle the regulatory complexity and technical integration required to support it.

Rwa prime brokerage 2026 choices that change the plan

The RWA market has expanded past $10 billion in 2026, driven by a tenfold growth in tokenized assets. As capital flows into tokenized real estate, stocks, and bonds, the infrastructure supporting these assets must evolve. Prime brokerage services now act as the critical bridge between traditional finance (TradFi) compliance and decentralized finance (DeFi) liquidity. Selecting the right prime broker requires evaluating specific tradeoffs that impact capital efficiency, regulatory safety, and operational speed.

Collateral Efficiency and Asset Acceptance

The value of a prime broker is often measured by what they will accept as collateral. Traditional FCMs typically require high-quality liquid assets like Treasuries or cash. RWA-focused prime brokers, however, may accept tokenized real estate, private credit, or equity as collateral for margin purposes. This flexibility allows for higher leverage on illiquid assets but introduces valuation risk. If the underlying asset is illiquid during a market stress event, liquidation can be difficult or delayed.

Regulatory Jurisdiction and Counterparty Risk

RWA prime brokerage operates in a fragmented regulatory landscape. A broker registered in Singapore or the Cayman Islands may offer broader access to Asian or institutional capital but provides less protection for US retail investors. Conversely, a US-registered prime broker ensures strict adherence to SEC and CFTC rules but may restrict access to certain DeFi protocols or high-yield tokenized products. The tradeoff is between regulatory safety and product breadth. Always verify the legal entity holding your assets and the segregation of client funds.

Technology Integration and Settlement Speed

DeFi liquidity relies on speed and programmability. A prime broker that integrates directly with on-chain settlement layers can offer near-instantaneous settlement, reducing counterparty exposure. Traditional prime brokers often rely on T+1 or T+2 settlement cycles, which can tie up capital. However, on-chain integration requires robust custody solutions. Evaluate whether the broker uses multi-signature wallets, MPC (Multi-Party Computation), or hardware security modules (HSMs) to manage private keys. The tradeoff here is between operational efficiency and custody security.

Cost Structure and Fee Transparency

Prime brokerage fees vary significantly based on the complexity of the assets. Tokenized assets may incur additional custody, oracle, and compliance fees compared to standard equities. Some brokers charge a flat monthly fee, while others take a percentage of assets under management (AUM) or trading volume. Be wary of hidden costs related to collateral haircuts or withdrawal fees. The most cost-effective option is not always the one with the lowest headline fee, but the one that minimizes capital drag through efficient collateral management.

| Feature | Traditional FCM | RWA Prime Broker |

|---|---|---|

| Collateral | Cash, Treasuries, Equities | Tokenized Real Estate, Private Credit, Equities |

| Settlement | T+1 or T+2 | Near-instant (on-chain) or T+1 |

| Regulation | Strict (SEC/CFTC/EU MiFID) | Varies (Cayman, Singapore, EU) |

| Leverage | Low to Moderate (2x-5x) | Higher (5x-10x) with haircut |

| Custody | Segregated Bank Accounts | MPC, HSM, or Multi-Sig Wallets |

How to choose a real-world asset prime broker

The RWA market has grown from under $1 billion to over $10 billion in 2026, with tokenized stocks and perpetuals seeing massive volume spikes. This growth brings complexity. You are no longer just buying an asset; you are navigating a hybrid plumbing system between traditional finance (TradFi) and decentralized finance (DeFi). Choosing the right prime broker is the most critical decision in this workflow.

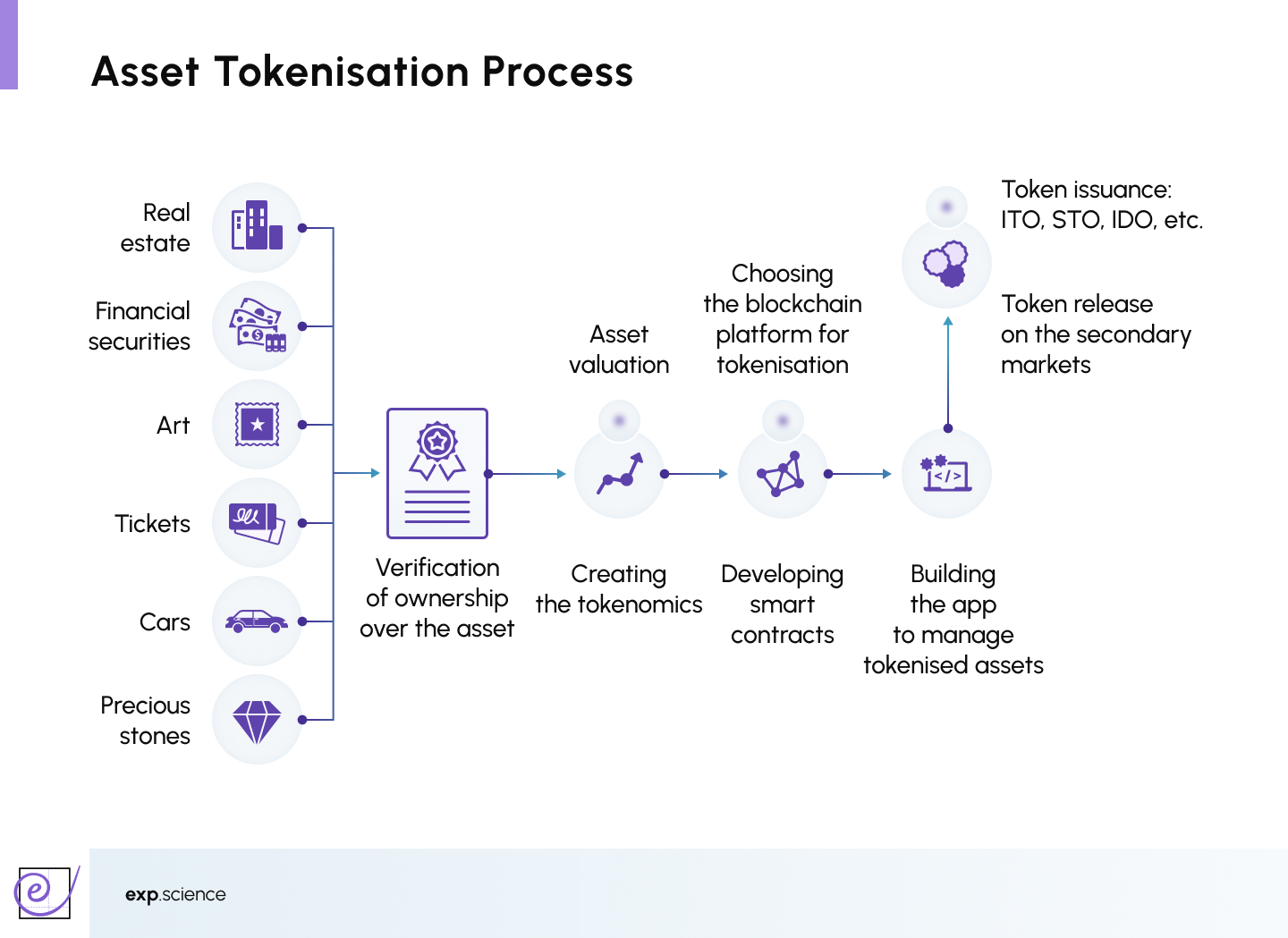

A prime broker does more than execute trades. They provide the credit lines, custody, and legal wrappers that allow on-chain assets to function like off-chain ones. Without them, you are exposed to smart contract risk and fragmented liquidity. Use this framework to evaluate your options.

The first check is legal. Ensure the broker is registered with the relevant authority for your location, such as the SEC, FCA, or MAS. RWA prime brokerage relies on legal ownership claims of the underlying asset. If the broker is unregulated, your claim to the real-world asset (like a treasury bill or real estate deed) may not hold up in court. Prioritize brokers with explicit licenses for both digital asset services and traditional brokerage.

Who holds the keys? Look for a hybrid custody model where the underlying asset is held in a segregated, audited account with a traditional bank, while the tokenized representation is held in a secure, multi-signature wallet. Check if the broker carries insurance for both the physical asset and the digital tokens. Self-custody solutions are rare in prime brokerage; if the broker offers "non-custodial" options, understand that you bear the full smart contract risk.

Prime brokerage is often about capital efficiency. Compare the loan-to-value (LTV) ratios offered against different RWA types. Treasury bills might offer 90% LTV, while real estate tokens may only offer 50%. Check the interest rates for borrowing against these assets. High leverage can amplify gains but also accelerates liquidation risk if the underlying asset price drops or if the tokenization protocol experiences a glitch.

How fast can you move? Traditional settlement takes T+2 days. A good RWA prime broker should offer near-instant on-chain settlement for the tokenized portion while handling the off-chain reconciliation in the background. Look for brokers that provide API access to their trading engines. This allows you to automate strategies and manage risk in real-time, rather than waiting for daily batch reports.

Transparency is the currency of trust. The broker should provide real-time proof of reserves for the underlying assets. This often means integrating with on-chain oracles that verify the balance of the custodial bank account. If the broker cannot provide a clear, auditable link between the token you hold and the asset in the vault, walk away. The $10 billion market growth is built on this new standard of verifiability.

The rise of RWA prime brokerage is not just a trend; it is a structural shift in how capital moves. By focusing on regulatory compliance, custody security, and operational transparency, you can navigate this space with confidence. The market is growing fast, but only the well-vetted players will survive the next phase of institutional adoption.

Spotting Weak Options in RWA Prime Brokerage

As the tokenized real-world asset (RWA) market surged past $10 billion in 2026, prime brokerage services have expanded to bridge traditional finance and decentralized liquidity. However, this rapid growth has attracted providers with misleading claims about risk mitigation and asset backing. Investors must distinguish between robust infrastructure and superficial tokenization.

Many platforms promise "instant liquidity" for illiquid assets like real estate or private credit. In practice, these pools often suffer from settlement delays or lack of secondary markets. A prime broker’s ability to provide true price discovery is more valuable than their marketing of high yields. Always verify the legal structure of the underlying assets and the custodial arrangements.

Another common pitfall is the conflation of financial market companies (FCMs) with full-service prime brokers. FCMs primarily handle execution and margining, while prime brokers offer lending, securities lending, and consolidated reporting. For sophisticated RWA strategies, understanding this distinction is critical to avoiding hidden costs and operational friction. The rise of RWA prime brokerage in 2026 demands rigorous due diligence on these service layers.

Rwa prime brokerage in 2026: common: what to check next

Real-world asset (RWA) prime brokerage is moving from experimental pilots to standardized infrastructure. As tokenized assets cross the $10 billion mark, investors face practical questions about market size, risk exposure, and execution structure. These answers address the most common objections before committing capital.

No comments yet. Be the first to share your thoughts!