RWA prime brokerage limits to account for

Use this section to make the decision on RWA prime brokerage easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have.

A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

RWA prime brokerage choices that change the plan

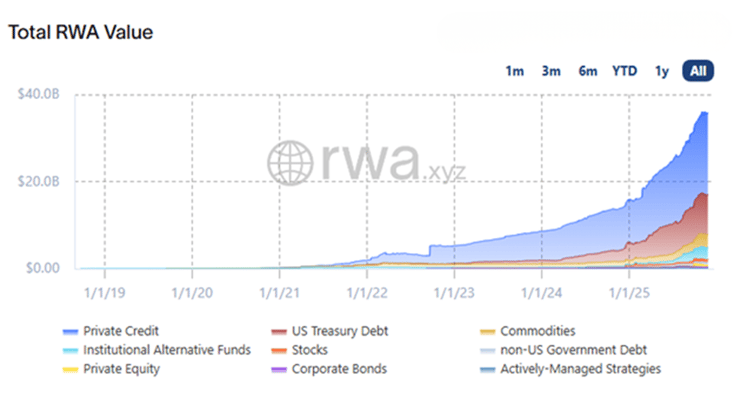

As institutional capital moves into tokenized real-world assets, the infrastructure supporting these trades must balance speed with regulatory rigidity. Prime brokerage for RWA is not just about settlement; it is about how capital constraints and counterparty risks are managed on-chain and off-chain. Evaluating these tradeoffs requires looking beyond yield to the mechanics of liquidity and risk weighting.

The following comparison highlights the core tradeoffs between traditional prime brokerage models and emerging RWA-native structures. Understanding these distinctions helps institutions determine which model fits their liquidity and compliance needs.

| Feature | Traditional Prime Brokerage | RWA-Native Prime Brokerage | Key Tradeoff |

|---|---|---|---|

| Capital Efficiency | High RWA charges (up to 100% for uncollateralized) | Lower RWA via on-chain collateral visibility | Visibility reduces capital costs but requires strict oracle reliability |

| Settlement Speed | T+2 or T+3 with manual reconciliation | Near-instant DvP (Delivery vs Payment) | Speed reduces counterparty risk but increases smart contract exposure |

| Liquidity Access | Deep pools in equities and fixed income | Fragmented liquidity across multiple chains | Chain-specific pools offer niche access but suffer from slippage |

| Regulatory Reporting | Standardized SWIFT and FIX protocols | On-chain audit trails with mixed compliance layers | Transparency aids audits but complicates cross-border data privacy |

Capital efficiency remains the primary driver for RWA adoption. In traditional finance, prime brokers face significant Risk-Weighted Asset (RWA) charges, particularly when assets lack perfect collateralization. A 100% RWA rating means the asset is treated as carrying standard credit risk, forcing banks to hold capital equal to the full asset value. RWA-native structures mitigate this by providing real-time, on-chain collateral visibility, allowing for more accurate risk weighting and potentially lower capital reserves.

However, this efficiency comes with a shift in risk profile. Traditional prime brokerage relies on established legal frameworks and centralized clearinghouses. RWA-native models replace some of this with smart contracts and oracles. While this reduces counterparty risk through atomic settlement, it introduces technology risk. Institutions must weigh the benefit of faster, cheaper settlement against the need for robust technical due diligence on the underlying blockchain infrastructure.

Liquidity fragmentation is another critical consideration. Traditional markets offer deep, consolidated order books. RWA markets are often siloed by asset type and blockchain network. This can lead to higher slippage and less predictable execution during market stress. The tradeoff here is access versus stability: RWA prime brokerage offers entry into previously illiquid asset classes but requires more sophisticated liquidity management strategies.

Key Evaluation Factors for RWA Prime Brokerage

-

Collateral Velocity

Assess how quickly collateral can be reused or rehypothecated on-chain to maximize capital efficiency. -

Oracle Reliability

Verify the redundancy and decentralization of price feeds, as errors can trigger automatic liquidations. -

Legal Wrapper Clarity

Ensure the legal link between the token and the underlying asset is enforceable across jurisdictions. -

Exit Liquidity

Test the depth of secondary markets for specific RWA tokens to ensure you can exit positions without significant price impact.

How to Choose the Right RWA Prime Broker

Institutional DeFi liquidity is no longer a speculative side bet; it is a balance sheet constraint. As banks tighten Risk-Weighted Asset (RWA) limits, hedge funds and pension funds must select prime brokers that can navigate these regulatory headwinds. The right partner doesn't just offer execution; they offer capital efficiency.

Choosing a prime broker for RWA strategies requires a shift from traditional volume metrics to regulatory agility. Here are the four critical factors to evaluate before committing capital in the 2026 market landscape.

Traditional prime brokers often treat tokenized assets as high-risk, applying steep haircuts or 100% RWA capital charges that tie up your balance sheet. Look for brokers who have secured regulatory clarity on specific asset classes, allowing for lower capital reserves. A broker that understands the difference between a fully collateralized stablecoin and an illiquid real estate token will offer you significantly more leverage.

Offchain settlement creates operational risk and settlement latency. The best RWA prime brokers integrate directly with the underlying blockchain rails, enabling atomic settlement where the asset and the cash change hands simultaneously. This reduces counterparty risk and ensures that your collateral is immediately usable for further trading, rather than sitting in a limbo state between traditional and digital ledgers.

Not all prime brokers are created equal when it comes to cross-border compliance. Ensure your broker holds the necessary licenses in the jurisdictions where your underlying assets are issued and where your fund is domiciled. A broker operating in a regulatory vacuum may offer lower fees, but they expose your institution to sudden compliance shocks. Prioritize firms with established relationships with central banks and financial conduct authorities.

In times of market stress, the speed of liquidation determines survival. Traditional prime brokers may take days to sell illiquid RWA positions, while onchain protocols can execute liquidations in seconds. However, speed without transparency is dangerous. Choose a broker that provides real-time visibility into your margin requirements and has clear, algorithmic liquidation protocols that prevent unfair price discovery during volatile periods.

The shift toward RWA prime brokerage is fundamentally about balancing yield with regulatory safety. By focusing on capital efficiency, settlement speed, and regulatory depth, institutions can realize the true potential of tokenized assets without overexposing their balance sheets to unnecessary risk.

Spotting Weak Options in RWA Prime Brokerage

As institutional DeFi liquidity reshapes 2026 markets, not every RWA prime brokerage claim holds up to scrutiny. Many platforms overstate their regulatory capital efficiency or hide restrictive covenants behind complex legal wrappers. To navigate this space, you must distinguish between genuine structural advantages and marketing fluff.

Here are three common pitfalls to avoid when evaluating RWA prime brokerage options:

The 100% RWA Misconception

A frequent misleading claim is that an asset is "100% RWA" because it is fully collateralized. In regulatory terms, this actually means the asset carries standard credit risk, forcing the bank to hold capital equivalent to the full amount of the asset. This eliminates any leverage benefit you might expect from prime brokerage financing. If a platform promises high returns based on "100% RWA" efficiency, they are likely misrepresenting the capital constraints. As noted by Finadium, banks are increasingly treating RWA as a primary binding constraint for assessing client business, meaning high RWA assignments directly limit the financing services available to hedge funds.

Hidden balance sheet limits to account for

Prime brokers affiliated with Global Systemically Important Banks (GSIBs) face strict balance sheet constraints. These limits restrict the maximum allowable RWA they can assign to their hedge fund clients. When a prime broker hits this ceiling, they may abruptly reduce liquidity or raise margin requirements without warning. This is not a market risk; it is a regulatory risk embedded in the prime brokerage agreement. Always verify whether the prime broker has sufficient regulatory capital headroom to support your specific RWA portfolio during market stress.

Misaligned Client Profiles

Another weak option arises when prime brokerage services are pitched to retail investors or small funds. Prime brokerage accounts are designed for institutional clients like pension funds and commercial banks that manage large cash volumes but lack internal investment management resources. These clients require sophisticated lending, securities lending, and clearing services that are cost-prohibitive for smaller players. If a platform targets retail investors with prime brokerage features, it is likely a repackaged margin lending product with higher fees and lower liquidity than true institutional prime brokerage.

RWA prime brokerage: common: what to check next

Before committing capital to RWA prime brokerage structures, it helps to separate the regulatory mechanics from the practical execution. Below are the most frequent questions from institutional investors evaluating these liquidity pools.

No comments yet. Be the first to share your thoughts!