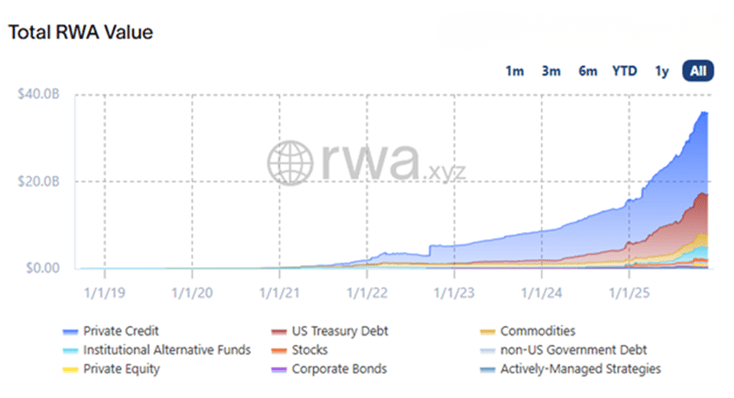

Tokenized asset market reaches $27.5 billion

The scale of real-world asset (RWA) tokenization has shifted from experimental pilots to institutional-scale deployment. By the first quarter of 2026, the total on-chain value of tokenized RWAs climbed to approximately $27.5 billion, a significant expansion from the $21 billion recorded at the start of the year. This growth trajectory underscores the increasing integration of traditional finance infrastructure with blockchain settlement layers.

For prime brokerage services, this volume creates a direct operational imperative. The rise in asset throughput demands custody solutions that can handle high-frequency settlement without compromising regulatory compliance. As the market matures, the friction between legacy clearing systems and digital asset rails becomes the primary bottleneck for leverage and liquidity provision.

Custody models: self-custody vs. prime

Institutional participation in real-world asset (RWA) tokenization requires a definitive choice between self-custody and prime brokerage. This decision dictates not only where the digital certificates of ownership reside but also how leverage is accessed and how regulatory liabilities are managed. Self-custody places the burden of security and compliance on the institution, while prime brokerage aggregates these functions to provide operational efficiency and credit lines.

The core trade-off centers on control versus capital efficiency. Self-custody offers maximum transparency and eliminates counterparty risk associated with a third-party custodian, but it demands significant infrastructure investment. Prime brokerage, conversely, allows institutions to leverage their tokenized assets against fiat or stablecoin loans, effectively turning static RWA holdings into active working capital. This model mirrors traditional hedge fund structures, where prime brokers facilitate lending and clearing services.

Custody Comparison

The following table contrasts the operational and financial implications of each model for institutional investors.

| Feature | Self-Custody | Prime Brokerage |

|---|---|---|

| Asset Control | Full private key management | Delegated to custodian |

| Leverage Access | Limited; requires separate lending agreements | Integrated credit lines and margin loans |

| Operational Overhead | High; internal security and compliance teams | Lower; outsourced custody and reporting |

| Counterparty Risk | Minimal (unless using third-party vaults) | Moderate; exposure to prime broker solvency |

| Regulatory Liability | Direct responsibility for KYC/AML | Shared; prime broker handles client onboarding |

| Liquidity Integration | Fragmented across multiple DEXs/CEXs | Aggregated liquidity pools and prime feeds |

Institutional Implications

For large asset managers, the prime brokerage model often presents a more viable path to scale. By integrating custody with lending, institutions can optimize their balance sheets without fragmenting their treasury operations. However, this convenience comes with the risk of commingling assets and potential restrictions on asset withdrawal during market stress.

Self-custody remains the preferred choice for entities with strict regulatory mandates or those requiring absolute isolation of assets. While the initial setup costs are higher, the long-term reduction in counterparty risk and operational fees can be significant for high-volume traders. The choice ultimately depends on the institution's risk tolerance and its need for leverage.

How leverage generates prime broker revenue

Prime brokerage functions as a capital intermediary, converting hedge fund balance sheets into institutional revenue. The primary mechanism is the extension of leverage, where the broker lends cash or securities against the fund's collateral portfolio. Every dollar of leverage deployed by a long/short fund creates a financing obligation for the prime broker, generating revenue through interest rate spreads and financing fees.

This lending activity is not merely a service but a core profit center. By borrowing funds at wholesale rates and lending them to hedge funds at a markup, prime brokers capture the spread between the two rates. This model scales directly with market volatility and fund asset growth; as funds increase their leverage to amplify returns, the prime broker's financing income rises proportionally. The relationship is symbiotic: funds require leverage to execute their strategies, and prime brokers require fund assets to deploy their balance sheets efficiently.

Rehypothecation controls and risk

Rehypothecation is the practice where a prime broker reuses client collateral to finance its own operations or lend to other clients. While this practice amplifies the prime broker's lending capacity and profitability, it introduces significant counterparty risk. If the prime broker defaults, clients may face delays or losses in recovering their original assets, as the collateral may have been pledged to third parties.

Institutional investors demand strict controls over rehypothecation. Most prime brokerage agreements include specific clauses limiting the percentage of collateral that can be reused, often capped at 140% of the value of the loans extended. However, the risk remains asymmetric. Unlike traditional banking deposits, prime brokerage collateral is not insured by the SIPC (Securities Investor Protection Corporation) or any government entity. In a bankruptcy scenario, clients become unsecured creditors, potentially recovering only a fraction of their assets.

The 2008 financial crisis highlighted these vulnerabilities. When Lehman Brothers collapsed, the rehypothecation of client assets complicated the recovery process for hedge funds, leading to prolonged legal battles and substantial losses. Today, institutional clients scrutinize prime broker balance sheets and rehypothecation policies more rigorously. The trend is toward greater transparency and stricter collateral segregation, with many funds opting for "no-rehypothecation" agreements despite the higher costs, prioritizing asset safety over financing efficiency.

Custody structures and collateral segregation

The structure of custody determines the level of protection afforded to client assets. Prime brokers typically offer two main custody models: omnibus accounts and segregated accounts. Each structure presents distinct trade-offs between operational efficiency, cost, and risk mitigation.

| Feature | Omnibus Account | Segregated Account |

|---|---|---|

| Collateral Location | Commingled in prime broker’s name | Held in client’s name at third-party custodian |

| Rehypothecation Risk | High – broker can reuse assets | Low – assets are ring-fenced |

| Cost | Lower financing fees | Higher custody and financing fees |

| Operational Complexity | Simplified for broker | Requires client coordination |

Omnibus accounts are the industry standard for most hedge funds due to their lower costs and operational simplicity. In this structure, all client assets are held in a single account under the prime broker’s name, allowing for efficient netting and rehypothecation. However, this efficiency comes at the cost of increased counterparty risk. Segregated accounts, while more expensive and complex, provide a higher degree of asset protection by holding collateral in the client’s name at an independent custodian. This structure minimizes the risk of asset loss in the event of prime broker default, making it preferable for funds with large, sensitive portfolios or those operating in highly regulated jurisdictions.

On-chain compliance standards in 2026

By 2026, the primary barrier to institutional RWA adoption is no longer technology, but regulatory clarity. The Securities and Exchange Commission (SEC) has shifted its focus from punishing early errors to defining the mechanics of programmable compliance. This transition is critical for prime brokerage services, where the ability to enforce transfer restrictions on-chain determines whether assets can be leveraged or settled efficiently.

In March 2026, SEC Commissioner Salman Banaei presented testimony before the House Financial Services Committee, outlining how blockchain technology can modernize capital markets. The testimony emphasized that compliance features—such as transfer restrictions and ownership registries—must be embedded directly into the asset’s smart contract logic. This approach ensures that every deposit, redemption, and transfer adheres to regulatory requirements without relying on manual off-chain checks.

The distinction between programmable and non-programmable assets is now the defining factor in custody and leverage. Programmable assets allow for automated compliance, reducing operational risk and enabling real-time settlement. Non-programmable assets, while more familiar, require intermediaries to enforce rules, creating friction and latency. This distinction is crucial for prime brokers who must balance regulatory adherence with operational efficiency.

The table below compares the operational implications of these two models for institutional prime brokerage services.

| Feature | Programmable Assets | Non-Programmable Assets |

|---|---|---|

| Transfer Restrictions | Enforced by smart contract logic | Enforced by off-chain intermediaries |

| Settlement Speed | Real-time or near-real-time | T+1 or T+2 with manual reconciliation |

| Operational Risk | Low (automated compliance) | High (manual intervention required) |

| Leverage Eligibility | High (transparent ownership) | Low (uncertain ownership chains) |

This shift toward programmable compliance is not just a technical upgrade; it is a regulatory imperative. As the SEC continues to refine its stance, institutions that fail to adopt on-chain compliance standards risk exclusion from prime brokerage services. The future of RWA custody lies in the ability to embed regulatory rules directly into the asset’s lifecycle.

Evaluating prime broker criteria

Selecting a prime broker for real-world asset (RWA) tokenization requires a rigorous audit of three pillars: liquidity depth, regulatory standing, and technical infrastructure. With the on-chain RWA market reaching approximately $27.5 billion in early 2026, institutions must ensure their prime service provider can handle this scale without compromising custody security or compliance reporting. The decision framework below outlines the essential criteria for evaluating providers.

Regulatory clarity is the primary filter. Providers must demonstrate explicit licensing or registration with relevant financial authorities (e.g., SEC, FCA) for both traditional securities and digital asset activities. Look for providers who have submitted formal written testimony or compliance frameworks to legislative bodies, such as the House Financial Services Committee. Avoid entities operating in regulatory gray areas, as this exposes the institution to counterparty risk and potential asset freezes.

Custody is not just about storage; it is about legal title and operational resilience. Evaluate whether the provider uses qualified custodians with segregated assets, multi-signature wallets, and cold storage solutions. The provider should offer clear proof of reserves and regular third-party audits. In the RWA context, ensure the custodian can handle both the digital token and the underlying legal entity structures (e.g., SPVs) that back the asset.

Liquidity depth determines your ability to enter and exit positions without significant slippage. Request detailed metrics on the provider’s market-making capabilities and access to traditional and decentralized liquidity pools. For leverage, scrutinize the loan-to-value (LTV) ratios, margin call thresholds, and haircuts applied to different RWA classes. Prime brokerage converts balance sheets into revenue; ensure the leverage terms are competitive and transparent, avoiding hidden fees that erode alpha.

The technical backbone must support high-frequency trading, real-time settlement, and seamless integration with your existing OMS/EMS. Assess the provider’s API latency, uptime history, and disaster recovery protocols. For RWA, the infrastructure must also support on-chain settlement layers and off-chain legal documentation updates. A robust technical stack reduces operational risk and ensures that trades execute exactly as intended, bridging the gap between traditional finance and blockchain.

| Feature | Traditional Prime | Crypto-Native Prime | Hybrid RWA Prime |

|---|---|---|---|

| Regulatory Coverage | Securities/FI focused | VASP/Digital asset focused | Dual-licensing required |

| Custody Model | Bank custody | Self-custody/MPC wallets | Segregated legal custody |

| Leverage Source | Bank balance sheet | DeFi lending pools | Hybrid capital sources |

| Settlement | T+2 days | Real-time/On-chain | Hybrid settlement layers |

-

Confirm dual licensing for securities and digital assets

-

Verify segregated custody with qualified third-party custodians

-

Review LTV ratios and margin call protocols for RWA classes

-

Audit API latency and on-chain settlement capabilities

-

Request recent third-party security and compliance audits

The most effective RWA prime brokers are those that bridge the gap between traditional financial rigor and blockchain innovation. By prioritizing regulatory clarity, secure custody, and robust technical infrastructure, institutions can manage the complexities of tokenized assets while minimizing risk.

No comments yet. Be the first to share your thoughts!